Rentvesting is a strategy that has been gaining traction among property investors in recent years. It allows individuals to rent a home in their desired location while investing in property in more affordable areas. This approach enables people to achieve their lifestyle goals as well as build a property portfolio at the same time. In this article, we explore the ins and outs of rentvesting and see why it’s becoming more popular among Australians.

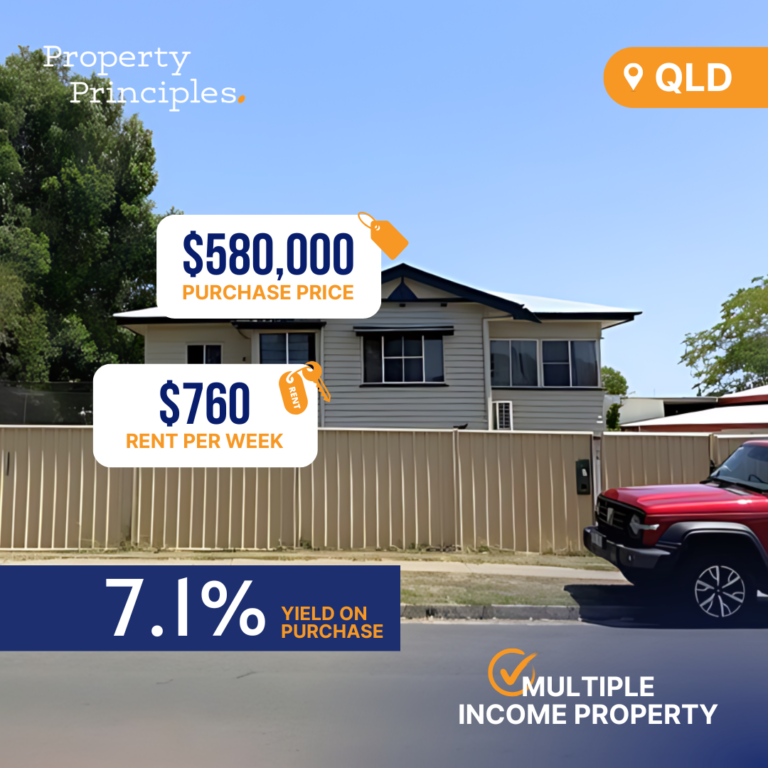

Take the example of Trevor Sanderson, a resident of Manly, who loves living by the beach in Sydney. Although he could never afford to buy an apartment in his building, which recently sold for a whopping $4.5 million, he can afford the weekly rent of $1050 and an investment property. Under the guidance of a property investment expert, he purchased a $570,000 dual-key apartment in south-east Queensland as part of his wealth creation strategy.

Rentvesting is becoming increasingly popular among those looking to enter the property market but faced with rising house prices. Experts predict that 30-40% of clients will choose rentvesting as their first step into property ownership.

One reason rentvesting is appealing is because it prioritizes lifestyle choices. Many rentvestors choose to live close to beaches, cafes, parks, or their workplaces for convenience and enjoyment. Renting in a central location also gives the flexibility to move around the country for job opportunities or a change of scenery.

Removing lifestyle needs from the property equation allows for more focused investing. Investors can concentrate on affordability, rental returns, and strong capital growth in their investments. By doing solid research or engaging a buyer’s advocate, investors can target high-growth areas that provide ample returns.

There are also potential tax savings with rentvesting. While living expenses are not tax-deductible for homeowners, the costs of holding an investment property might be. For instance, if the property is negatively geared, investors can often claim the losses against their other income. Additionally, property renovations and new appliances can be claimed as deductions, along with other related expenses such as mortgage interest and property management fees.

However, there are some drawbacks to consider with rentvesting. First home buyers may need to forgo government grants targeted at owner-occupiers, potentially missing out on thousands of dollars in funding. Additionally, capital gains tax will apply to the sale of an investment property, unlike the tax-free status of selling one’s own home.

One crucial aspect of rentvesting is that it needs to be a long-term proposition. Buyers should be prepared for a commitment of at least ten years to maximize the benefits and avoid the pitfalls of short-term investing, such as hefty costs like stamp duty, agent fees, and capital gains tax.

To sum up, rentvesting is a flexible and appealing strategy for many Australian property investors. It enables individuals to live in their desired location while building a property portfolio in more affordable areas. While there are some drawbacks, such as missing out on government grants and having to pay capital gains tax, the benefits of rentvesting can outweigh these challenges for those who are prepared for a long-term investment. Therefore, if you’re considering diving into the property market but want to enjoy your lifestyle simultaneously, rentvesting could just be the perfect solution for you.